When you sit down to buy your first home, your mind is likely racing with thoughts of paint colors, school districts, and packing boxes. Most people don't immediately think about their golden years. However, homeownership is an instrumental part of a healthy retirement plan.

As a leading mortgage broker in Southington, CT, the team at New England Home Mortgage has seen firsthand how a well-structured mortgage can set families up for long-term financial freedom. Every time you make a mortgage payment, you are effectively forcing yourself to save. You are building equity—a critical asset that can be tapped into later in life.

By starting with a solid pre-qualification, you can ensure your home purchase aligns with both your current budget and your future retirement goals.

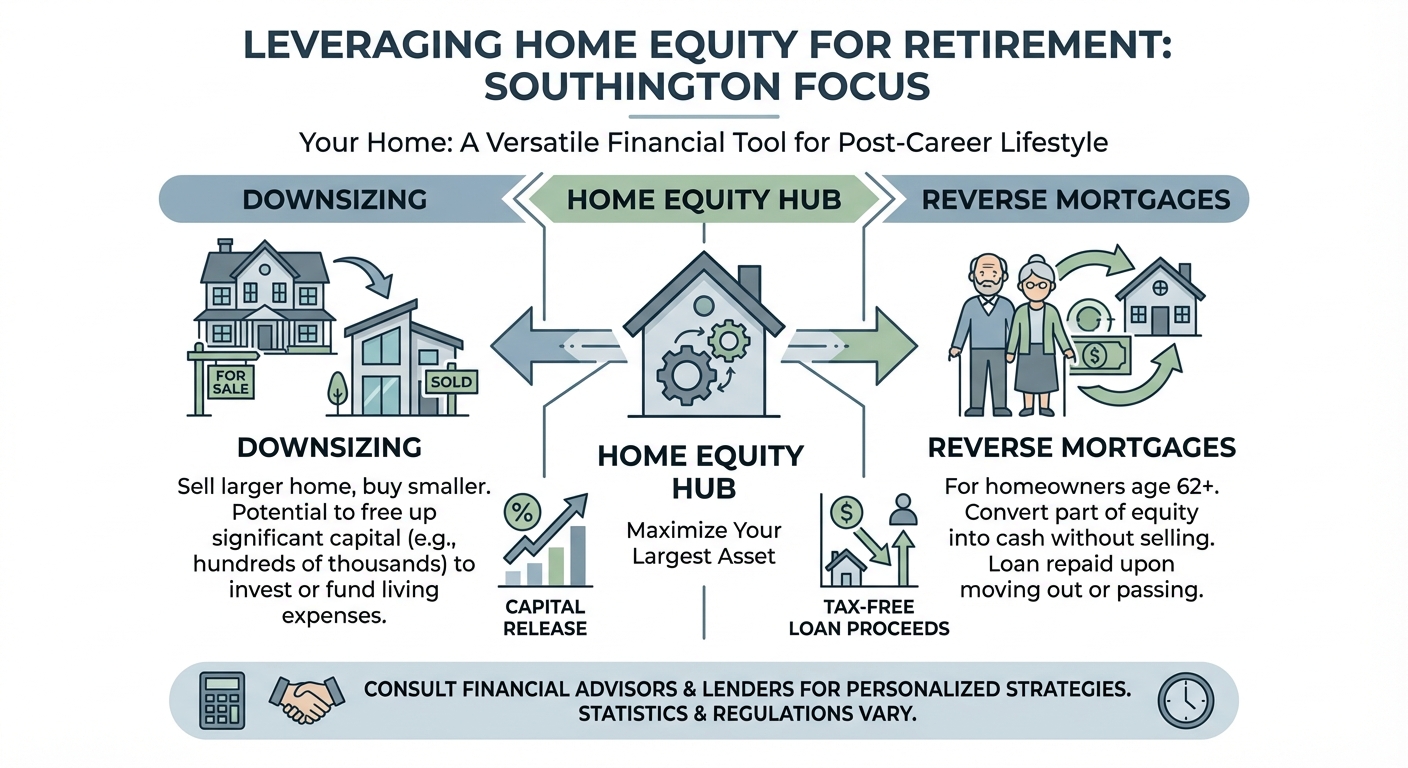

As you approach retirement age, the equity you've built in your Connecticut home becomes a highly versatile financial tool. Many retirees find that their home is their largest single asset, offering multiple avenues to fund their post-career lifestyle.

Consider these powerful ways to leverage your home for retirement:

At New England Home Mortgage, we focus on people first. Brian Taylor and our expert team will help you explore all available mortgage options to ensure your home works for you, not the other way around.

A healthy retirement plan doesn't happen by accident; it requires strategic decisions early on, especially regarding real estate. Whether you are buying your first home or refinancing your current one, having a trusted local advisor makes all the difference.

As a five-time winner of the Five Star Professional Award, New England Home Mortgage is dedicated to making the loan process stress-free. We take pride in learning your personal financial situation and taking the time to explain your options.

Don't wait until your golden years to think about how your home fits into your retirement picture. Let us help you secure a mortgage that builds your wealth today for a secure tomorrow.

Q1: How does buying a home help with retirement planning?

Buying a home acts as a forced savings plan. As you pay down your mortgage, you build equity. By the time you retire, you may have a paid-off home, significantly reducing your living expenses, or a valuable asset you can sell or borrow against.

Q2: Should I pay off my mortgage before I retire?

For many, entering retirement without a monthly mortgage payment provides immense peace of mind and reduces the income needed to cover daily expenses. However, it is best to consult with a financial advisor and your mortgage broker to determine what makes the most sense for your specific portfolio.

Q3: What if I buy my first home later in life?

It is never too late to start building equity. Even if you don't pay off the 30-year mortgage entirely before retiring, you are still stabilizing your housing costs against inflation and building an asset that can be passed on or sold.

Q4: Can I use my home equity to fund my retirement?

Yes! You can downsize and keep the profit, take out a Home Equity Line of Credit (HELOC), or utilize a reverse mortgage to convert your home's equity into usable cash without having to move.

Q5: How do I get started with a mortgage in Southington, Simsbury, Madison, Guilford, Fairfield or anywhere in Connecticut?

Getting started is easy. Contact Brian Taylor at New England Home Mortgage or fill out our online pre-qualification form. We will review your financial situation and find the best loan options tailored to your long-term goals.

Call Brian Taylor at 1 (860) 798-7289 or email brian@brianct.com to discuss your future.

Apply Now with New England Home Mortgage