As we move through 2026, the housing market is witnessing a welcome stabilization in mortgage rates, creating new opportunities for homeowners. After the volatility of previous years, many residents in Southington, CT, and the greater Connecticut area are finding themselves in a prime position to revisit their current home loan rates. Refinancing now could mean significantly lowering your monthly payments, shortening your loan term, or tapping into your home's equity for renovations or debt consolidation.

At New England Home Mortgage, we understand that timing is everything. With the market settling, locking in a rate this year could save you tens of thousands of dollars in lifetime interest over the life of your loan. Whether you purchased your home during the peak rate periods or have built up substantial equity over the last few years, evaluating your options with a local expert is the first step toward financial optimization.

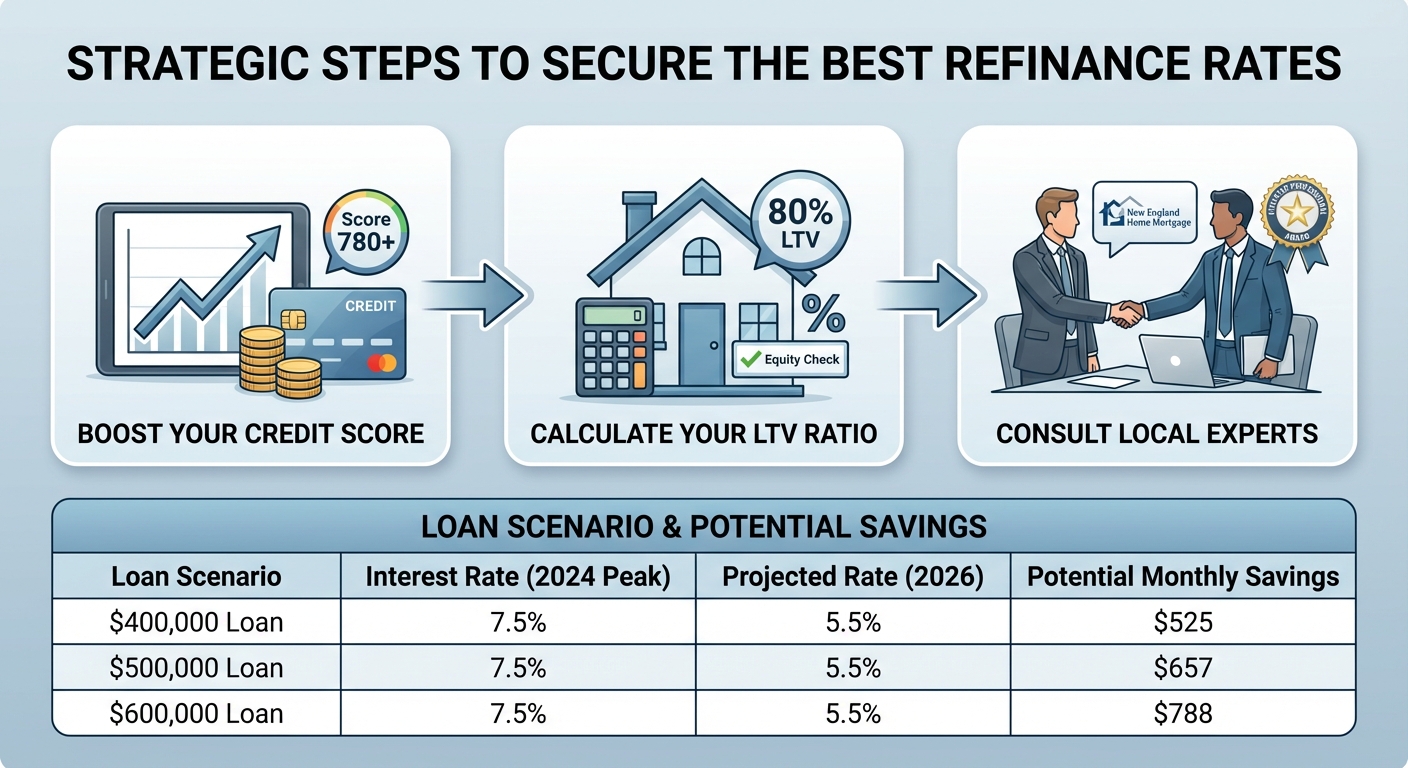

Securing the best possible rate requires more than just watching the market; it requires preparation. Lenders in 2026 are looking for stability and strong financial health. Here are key strategies to ensure you get the most competitive offer:

Refinancing is a significant financial decision, and having a trusted partner makes all the difference. New England Home Mortgage focuses on a "client first" approach. We know the process can seem overwhelming, which is why we have streamlined our loan process to be as stress-free as possible. From pre-qualification to closing, our team builds relationships founded on trust and communication.

Don't just take our word for it. Clients like Kyle and Katie, first-time homebuyers, noted, "The entire New England Home Mortgage team were amazing throughout the entire process... We would recommend them to anyone looking for the BEST Mortgage experience." Whether you are new to home ownership in Cheshire, or a long-time homeowner in Southington, we are committed to finding the loan product that specifically meets your unique needs.

Q1: What are the benefits of refinancing in 2026?

Refinancing in 2026 allows you to take advantage of stabilizing rates to lower your monthly payment, reduce your interest costs, or cash out equity for major expenses.

Q2: How long does the refinancing process take with NEHM?

While timelines vary based on complexity, our streamlined loan process typically allows us to close refinances in under 30 days.

Q3: Do I need a new appraisal to refinance?

In many cases, yes, to determine the current market value of your home. However, many loan programs may offer appraisal waivers depending on your home equity and credit profile. FHA, for example, offers a streamlined refinance that does not require an appraisal given certain requirements are met.

Q4: Can I refinance if I have a government-backed loan?

Absolutely. We specialize in FHA, VA, and USDA refinancing options, including streamline refinances that require less documentation.

Q5: Is there a cost to get a quote?

No, getting a pre-qualification or a rate quote from New England Home Mortgage is free and comes with no obligation.

Contact Brian Taylor at New England Home Mortgage Today to Start Your Refinance